U.S. Corporate Tax Rate History

Reviewed by Josh for financial modeling and data. See more by Josh.

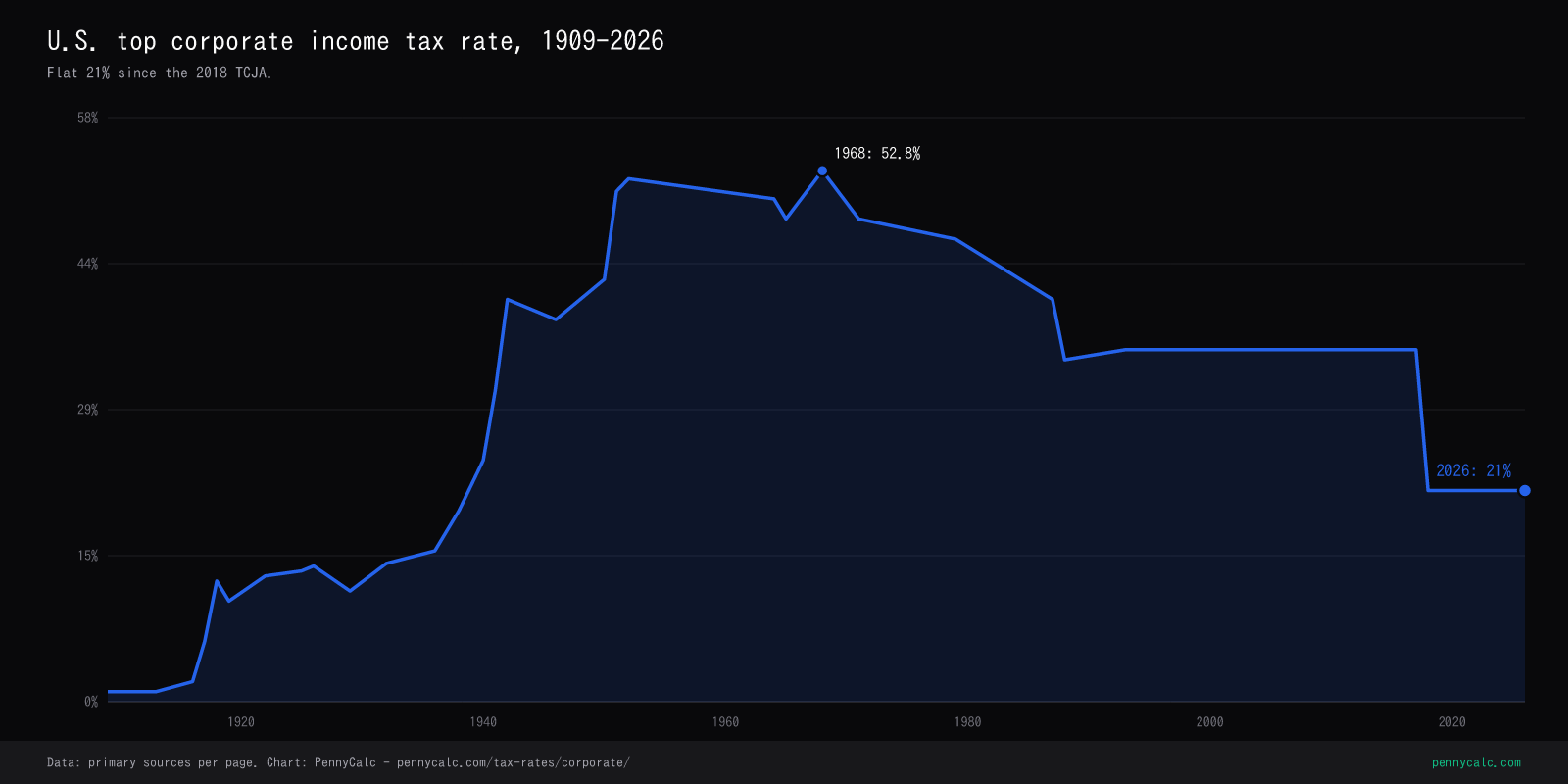

The top federal corporate income tax rate from 1909 to 2026, with every major tax act annotated.

Sources: IRS Statistics of Income, Tax Foundation, Joint Committee on Taxation

Download this chart: PNG light · PNG dark - PennyCalc chart artwork is reusable under CC BY 4.0 with attribution; source-data terms still apply. Licensing details.

{kind=link}

{kind=link}

The major corporate tax acts

Six legislative milestones drove the line on the chart above.

Corporation Excise Tax Act of 1909 - the federal corporate tax begins

Four years before the personal income tax, Congress passed the Corporation Excise Tax - a 1% levy on corporate net income above $5,000. It was structured as an "excise tax on the privilege of doing business as a corporation" specifically to dodge the constitutional issues that had killed the personal income tax in 1895. The Supreme Court upheld it in Flint v. Stone Tracy Co. (1911), and the modern corporate tax was born.

WWII transforms the corporate tax - and adds the excess-profits tax

The Revenue Act of 1942 raised the regular corporate rate to 40% and layered a separate excess-profits tax on top - peaking at 95% on profits above a "normal" return. Combined effective rates for war contractors regularly exceeded 80%. The excess-profits tax was repealed in 1946 but reinstated for the Korean War (1950-1953), then permanently retired.

The high-rate era - 48-52% as the norm for three decades

From 1951 through 1986, the top federal corporate rate hovered between 46 and 52 percent. State corporate taxes added another 5-10 points on average. Combined statutory rates of 50-60 percent were normal for that entire generation of US corporate executives - yet effective rates were dragged well below the headline by depreciation rules, investment tax credits, and the foreign tax credit.

TRA86 - the great corporate base-broadening

The Tax Reform Act of 1986 cut the corporate rate from 46% to 34% in stages, but financed the cut by killing the investment tax credit, lengthening depreciation schedules, and tightening the foreign tax credit. The combined effect was that corporate tax revenue actually rose in the years following TRA86 even though the headline rate fell. It remains one of the cleanest examples of base-broadening rate-lowering reform in U.S. history.

OBRA 1993 - the bump to 35%

Clinton-era OBRA raised the top corporate rate from 34% to 35% and added a new top bracket structure. The 35% headline persisted for 24 straight years (1993-2017) - the longest unchanged corporate top rate in modern U.S. history.

TCJA - the slash to 21% (and made permanent)

The Tax Cuts and Jobs Act of 2017 cut the corporate rate from 35% to a flat 21% effective January 1, 2018 - the largest single corporate rate cut in U.S. history. Unlike the individual provisions of TCJA, which were scheduled to sunset, the 21% corporate rate was made permanent. The cut also moved the U.S. from a worldwide to a quasi-territorial system via the new GILTI and FDII regimes.

Headline vs. effective: why the line tells half the story

The headline corporate rate is the rate on taxable income at the top bracket. The effective rate is total tax paid divided by book income - and it has consistently run lower than the headline:

- 1950s peak: 52% headline, ~30% effective for the largest firms (investment tax credits, depreciation, foreign income deferral)

- Late 1980s: 34% headline, ~30% effective (TRA86 closed many shelters; the gap narrowed)

- 2010s: 35% headline, ~22% effective for the S&P 500 (foreign income deferral, R&D credit, NOL carryforwards)

- Post-TCJA: 21% federal statutory rate; reported effective rates vary by company, period, tax base, and treatment of credits, deductions, foreign income, and state taxes

The shrinking headline-to-effective gap is itself a TRA86 legacy: every major reform since has been "lower the rate, broaden the base," which compresses the difference between statutory and economic.

Frequently Asked Questions

What was the highest U.S. corporate tax rate ever?

When was the corporate tax rate at its lowest?

Did corporations actually pay the 50%+ rates in the 1950s-1980s?

How does the 21% U.S. corporate rate compare internationally?

What's the difference between the corporate rate and what corporations actually pay?

Why didn't TCJA's corporate cut sunset like the individual cuts did?

Related Calculators

Personal Tax Brackets History (1913-2026)

Top marginal personal income tax rate chart with every major tax act annotated.

Capital Gains Tax Rate History

Top long-term capital gains rate from 1922 through ATRA + ACA NIIT.

Capital Gains Calculator

Short and long-term cap gains, NII surtax, net proceeds.

Self-Employment Tax Calculator

SE tax, estimated quarterly payments for freelancers and S-corp owners.

Educational content only. Historical rates apply only to the years shown. State corporate taxes add 0-12% on top of federal depending on jurisdiction. Consult a qualified CPA or tax attorney for entity-specific planning.