IRA Contribution Limit History

Last verified: July 12, 2026 against IRS Revenue Procedures + ERISA/EGTRRA/SECURE legislative history

Reviewed by Josh for financial modeling and data. See more by Josh.

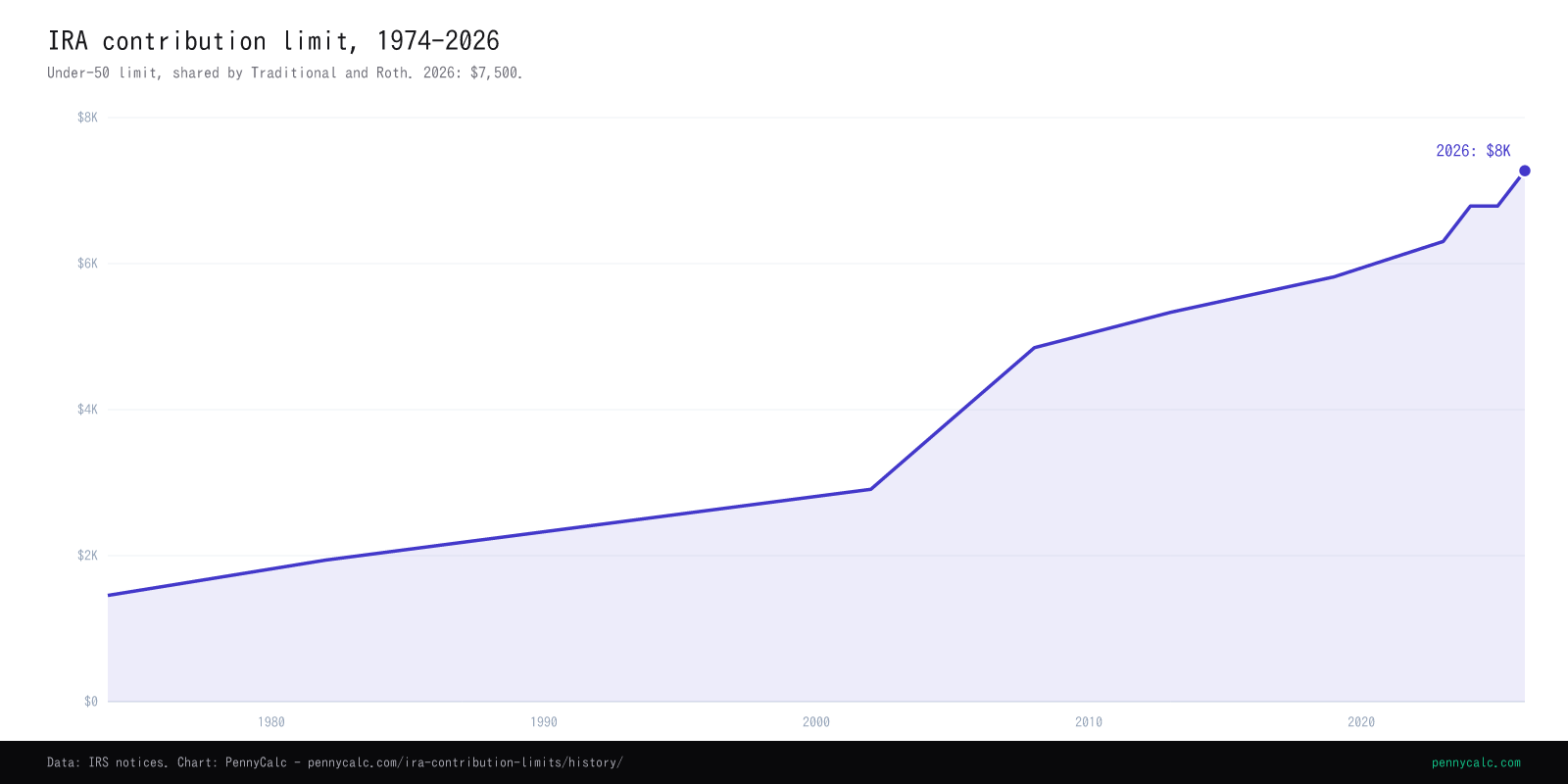

The annual IRA limit from $1,500 in 1974 to $7,500 in 2026, including the 20-year freeze at $2,000 and the slow arrival of catch-up contributions.

Sources: IRS Revenue Procedures, the Internal Revenue Code legislative history, and IRS Notice 2025-67 for 2026. Figures are the combined Traditional and Roth limit.

Download this chart: PNG light · PNG dark - PennyCalc chart artwork is reusable under CC BY 4.0 with attribution; source-data terms still apply. Licensing details.

{kind=link}

{kind=link}

The major changes

The IRA limit has moved in three distinct eras: a low fixed amount in the 1970s, a famous 20-year freeze at $2,000, and a post-2002 period of scheduled increases and inflation indexing. The rules around the account changed more than the dollar figure did.

ERISA creates the IRA at $1,500

The Employee Retirement Income Security Act of 1974 created the Individual Retirement Arrangement, with a contribution limit of $1,500 or 15% of earned income, whichever was less. It was originally available only to workers who were not covered by an employer pension plan. The idea was to give people without a company pension a tax-favored way to save on their own.

ERTA opens the IRA to everyone and raises the limit to $2,000

The Economic Recovery Tax Act of 1981, effective in 1982, opened IRA eligibility to every worker regardless of pension coverage and raised the limit to $2,000. Contributions boomed. This is the period that built the IRA into a mainstream retirement vehicle, and the $2,000 figure became fixed in the public mind because it then did not move for two decades.

Tax Reform limits the deduction for the pension-covered

The Tax Reform Act of 1986 kept the $2,000 limit but reintroduced income-based phaseouts on the deduction for workers (and spouses) covered by a workplace plan. You could still contribute, but high earners with a 401(k) lost the up-front deduction. This split the IRA into deductible and nondeductible contributions and laid the groundwork for the later backdoor Roth, which relies on nondeductible contributions.

The Roth IRA launches

The Taxpayer Relief Act of 1997 created the Roth IRA, effective 1998. It shared the same annual dollar limit as the Traditional IRA, so the two have always drawn from one combined cap rather than separate ones. The Roth flipped the tax treatment: no deduction up front, but tax-free growth and withdrawals. The combined-limit structure is why you cannot contribute the full amount to both a Traditional and a Roth in the same year.

EGTRRA raises limits on a schedule and adds catch-up contributions

After two decades frozen at $2,000, the 2001 EGTRRA set a step-up schedule: $3,000 for 2002 through 2004, $4,000 for 2005 through 2007, and $5,000 in 2008, after which the limit would be indexed to inflation in $500 increments. EGTRRA also introduced the age-50 catch-up contribution, starting at $500 and rising to $1,000 by 2006. This was the first time older savers could put in more than younger ones.

The SECURE Act repeals the age cap and ends the stretch IRA

The SECURE Act of 2019, effective 2020, removed the rule barring Traditional IRA contributions after age 70.5, letting older workers keep contributing. In the same law, Congress paid for that by ending the stretch IRA: most non-spouse heirs must now empty an inherited IRA within 10 years rather than over their own lifetimes. The contribution limit did not change, but the rules around the account did, significantly.

SECURE 2.0 indexes the catch-up, and the limit reaches $7,500

The base limit rose to $7,000 for 2024 and stepped to $7,500 for 2026 (IRS Notice 2025-67), with the age-50 catch-up at $1,100. SECURE 2.0 finally indexed the catch-up to inflation starting in 2024, after it had been frozen at $1,000 since 2006; 2026 is the first year the indexing actually moved it.

Things you might not know

- The 20-year freeze cost more than it looks. Holding the limit at $2,000 from 1982 to 2001 meant the cap lost about half its purchasing power to inflation over that period. A saver who maxed out every year contributed the same nominal $2,000 in 2001 that, in real terms, was worth far less than the $2,000 of 1982. The post-2002 indexing exists specifically to prevent that slow erosion from happening again.

- The catch-up was frozen almost as long. The $1,000 age-50 catch-up reached that level in 2006 and stayed there through 2025. SECURE 2.0 indexed it beginning in 2024, and the rounded amount first increased in 2026 to $1,100.

- The combined limit blocks a common assumption. Many people assume they can put $7,000 in a Traditional IRA and another $7,000 in a Roth. They cannot. The limit is the total across both. The only way to get more than the IRA limit into a Roth is through a Roth 401(k) or a backdoor or mega-backdoor strategy, which rely on different parts of the code.

- Nondeductible contributions created the backdoor Roth. The 1986 reform that limited the deduction for pension-covered workers left them able to make nondeductible Traditional contributions. Decades later, after Congress removed the income cap on Roth conversions in 2010, those nondeductible contributions became the basis of the backdoor Roth: contribute nondeductible, then convert. A rule meant to limit a benefit ended up enabling a workaround.

- The end of the stretch IRA was the price of other changes. The SECURE Act\'s headline was friendly, letting people contribute past 70.5 and delaying required distributions. The revenue to pay for it came from forcing most inherited IRAs to be emptied within 10 years, which can push a working-age heir\'s income into a much higher bracket during their peak earning years. The contribution rules got easier; the inheritance rules got harder.

What the limit does and does not decide

The annual contribution limit is only one part of an IRA decision. Account eligibility, whether a traditional contribution is deductible, the choice between pretax and Roth treatment, and the pro-rata rule for Roth conversions can matter more to the after-tax result. Conversion timing, asset location, and the SECURE Act's inherited-account rules also affect a long-term projection. Use the published limit as an input, then compare the tax treatment against the marginal rate today and the rate reasonably expected in retirement.

IRA contribution limit by year

The combined Traditional and Roth under-50 limit from 1974 to 2026. Years not listed held the prior limit, including the well-known freeze at $2,000 from 1982 through 2001. For 2026, the age-50 catch-up adds $1,100.

| Year | IRA contribution limit | What changed that year |

|---|---|---|

| 1974 | $1,500 | ERISA creates the IRA with a $1,500 annual limit for workers without a pension |

| 1982 | $2,000 | ERTA opens the IRA to everyone and raises the limit to $2,000 |

| 2002 | $3,000 | EGTRRA raises limits on a schedule and adds the age-50 catch-up |

| 2005 | $4,000 | |

| 2008 | $5,000 | |

| 2013 | $5,500 | |

| 2019 | $6,000 | |

| 2023 | $6,500 | |

| 2024 | $7,000 | SECURE 2.0 indexes the $1,000 catch-up to inflation |

| 2025 | $7,000 | |

| 2026 | $7,500 |

Full series shown. Scroll within the table to see every year.

Frequently Asked Questions

What is the 2026 IRA contribution limit?

Is the IRA limit the same for Traditional and Roth?

Why was the IRA limit stuck at $2,000 for so long?

When did catch-up contributions start?

What is the difference between the IRA limit and the 401(k) limit?

Can I still contribute to an IRA after age 70?

To put the limit to work, project a balance with the Roth IRA calculator or run the Roth vs Traditional comparison. For the larger workplace cap, see the 401(k) contribution limit history. For sources and update cadence, see our methodology.

Related Calculators

Roth IRA Calculator

Project a Roth balance with the 2026 limit and MAGI phaseouts.

Roth IRA vs Traditional IRA

Apples-to-apples after-tax comparison of the two account types.

Roth IRA Limit History

The Roth-specific contribution and phaseout history since 1998.

401(k) Contribution Limit History

The employee deferral limit since 1987, a separate and larger cap.

Retirement Calculator

Project accumulation and drawdown across all your accounts.

Methodology

How we source and verify every rate, limit, and bracket.

Educational content only. Contribution limits, phaseouts, and deduction rules are set by the IRS and change annually; the 2026 limit is from IRS Notice 2025-67. Consult a qualified tax advisor for decisions specific to your situation.