Medicare Part B Premium History

Last verified: July 19, 2026 against CMS final 2026 Part B premium, deductible, and IRMAA announcement + historical CMS notices

Reviewed by Josh for financial modeling and data. See more by Josh.

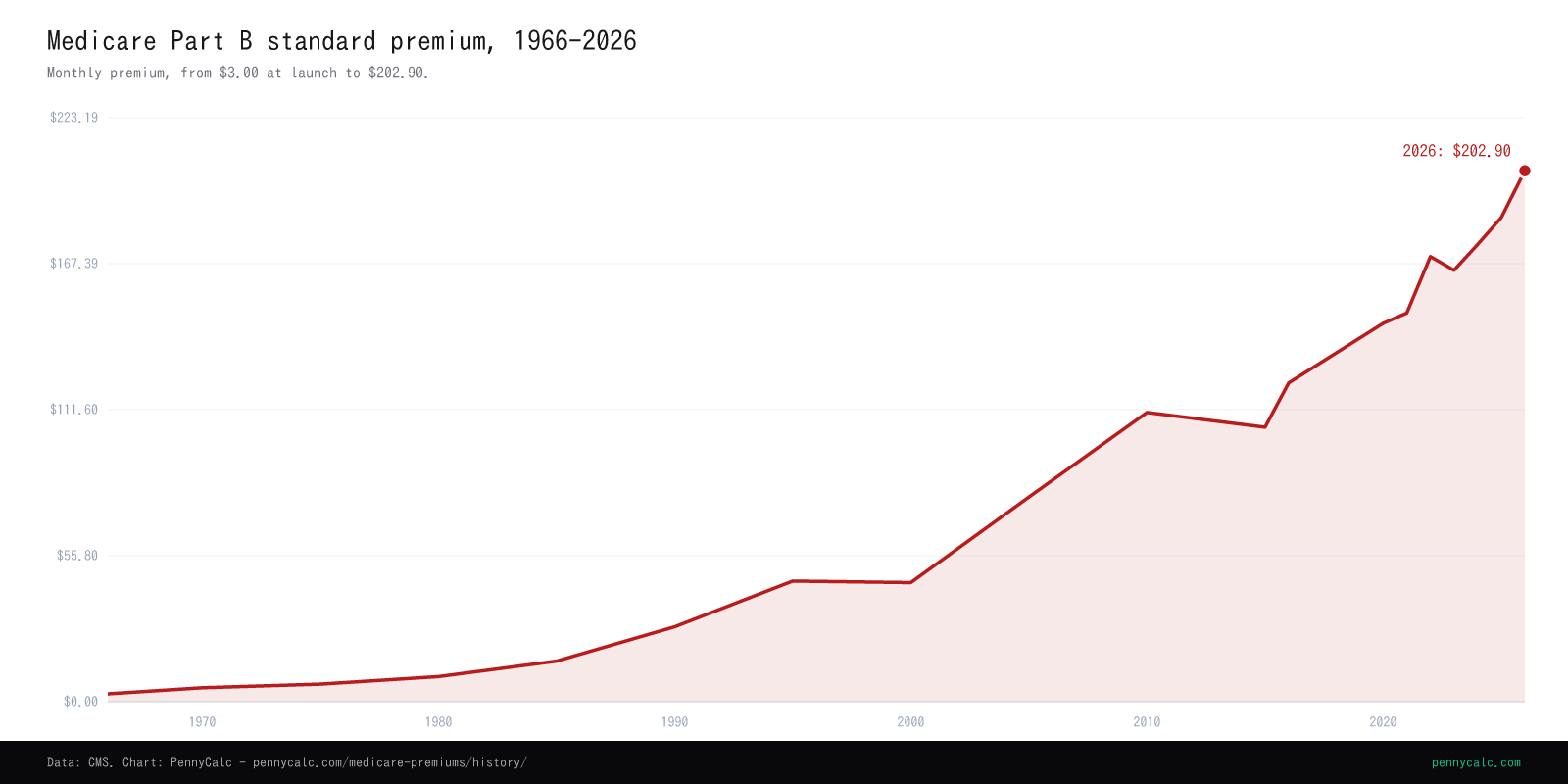

The standard Part B premium from $3.00 a month in 1966 to $202.90 in 2026, and how IRMAA income surcharges layered on top since 2007.

Sources: CMS annual Part B premium, deductible, and IRMAA announcements; Medicare Trustees Reports; and the legislative history for IRMAA.

{kind=link}

{kind=link}

The major changes

Two stories run through this chart. The first is steady premium growth, faster than general inflation, driven by rising outpatient and physician spending. The second is the layering of income-related surcharges since 2007, which turned a single flat premium into a tiered system that high earners navigate carefully.

Part B launches at $3.00 a month

The 1965 Social Security Amendments created Medicare. Part A (hospital insurance) was funded by payroll taxes, but Part B (outpatient and physician coverage) was voluntary and funded partly by a monthly premium. The original premium was $3.00 a month, set to cover half of Part B costs, with general federal revenue covering the other half. Enrollment was optional then and remains so today, though most people enroll because delaying triggers a permanent late-enrollment penalty.

The premium is pegged to 25% of program cost

A 1972 amendment limited how fast the premium could rise, tying its growth to the Social Security COLA rather than to actual Part B cost growth. By the early 1980s the premium had fallen to around 25% of program cost, with general revenue covering the remaining 75%. The 1982 and 1983 budget acts formalized the 25% rule: the standard premium is set each year to cover roughly a quarter of expected Part B spending per enrollee. That 75% general-revenue subsidy is why Part B is a better deal than its sticker price suggests.

IRMAA arrives for high-income enrollees

The 2003 Medicare Modernization Act introduced the Income-Related Monthly Adjustment Amount, or IRMAA, effective 2007. For the first time, higher-income enrollees paid a surcharge on top of the standard premium, scaled so the highest earners covered closer to 80% of their own Part B cost rather than 25%. The surcharge applied in tiers based on modified adjusted gross income, using the income reported two years earlier. A 2007 retiree paid IRMAA based on their 2005 tax return.

Part D gets its own IRMAA surcharge

The Affordable Care Act extended IRMAA to Medicare Part D (prescription drug coverage) starting in 2011. High earners now pay two separate income surcharges: one added to the Part B premium and a second added to whatever Part D plan premium they choose. The Part D surcharge is paid to Medicare directly, not to the drug plan, which surprises enrollees who assume their plan premium is the whole bill.

A fifth, steeper tier is added at the top

The 2015 Medicare Access and CHIP Reauthorization Act (MACRA) added a fifth IRMAA tier effective 2018, hitting the highest incomes (above $500,000 single and $750,000 married in current figures) with the steepest surcharge. Before 2018 the top tier started lower and was less steep. This change specifically targeted very high earners and is the tier most likely to catch retirees in a one-time income spike from a business sale or large Roth conversion.

The income brackets finally get indexed to inflation

From 2007 through 2019 the IRMAA income thresholds were frozen in nominal dollars, with one exception. That freeze pulled a growing share of middle-income retirees into surcharge territory each year as ordinary inflation lifted their incomes past static thresholds. The 2018 Bipartisan Budget Act indexed the brackets to inflation starting in 2020, so the thresholds now rise each year with the CPI. The top tier remains unindexed by design.

The premium actually falls, by 3%

In 2022 CMS set an unusually large premium increase, to $170.10, partly to build a reserve for Aduhelm, a newly approved Alzheimer's drug expected to cost Medicare billions. When Aduhelm's price was cut and coverage was restricted, the reserve proved unnecessary. CMS responded by lowering the 2023 premium to $164.90, one of the only year-over-year decreases in Part B history. It is a useful reminder that the premium reflects projected program cost, not a one-way ratchet.

Where premiums stand today

CMS set the standard 2026 Part B premium at $202.90 a month, up from $185.00 in 2025, and the annual deductible at $283.00. At the top 2026 IRMAA tier, the Part B surcharge is $487.00 and the total Part B premium is $689.90 per person per month.

Things you might not know

- The IRMAA brackets were frozen for 12 years. From 2007 to 2019 the income thresholds stayed fixed in nominal dollars. A retiree whose income rose only with inflation could drift into a surcharge tier they would not have hit in 2007. Indexing began in 2020, but the freeze quietly widened IRMAA's reach across the entire 2010s.

- The top tier is still not indexed. When the brackets were indexed in 2020, the highest tier (above $500,000 single and $750,000 married) was deliberately left frozen. Its real threshold falls a little every year, so over time more high earners land in the steepest bracket.

- The surviving-spouse penalty is real and abrupt. When one spouse dies, the survivor files as single the following year. The married IRMAA thresholds are roughly double the single thresholds, so the same total income that sat comfortably below a bracket while married can trigger a surcharge once the survivor files single. This is sometimes called the widow's penalty, and it stacks with the loss of one Social Security check.

- A hold-harmless provision protects most beneficiaries from premium spikes. For enrollees who have Part B premiums deducted from their Social Security checks, the dollar increase in the Part B premium generally cannot exceed the dollar amount of their COLA. In a low-COLA year this caps the premium increase for most people, shifting more of the rise onto new enrollees and IRMAA payers, who are not protected.

- IRMAA is the rare federal surcharge with a real appeal path. Form SSA-44 lets you ask Social Security to recompute IRMAA on more recent income after a life-changing event such as retirement. Many newly retired enrollees overpay in their first Medicare year simply because no one told them the form exists; their final working year's income sets the surcharge, and the appeal resets it.

A note on planning around the brackets

IRMAA planning differs from ordinary income-tax planning because Medicare generally uses modified adjusted gross income from the tax return filed two years earlier. A Roth conversion or other income event can therefore affect a later Medicare premium even when it fits within the intended federal tax bracket. Compare a proposed conversion with both the tax brackets for the conversion year and the IRMAA tiers for the Medicare year that income may determine. Because the surcharge changes by tier, income near a threshold deserves a separate calculation. Qualifying life-changing events may support an appeal using Form SSA-44.

Standard Part B premium by year

The standard monthly Part B premium before any IRMAA surcharge, from $3.00 in 1966 to $202.90 in 2026. Years not listed held close to the prior year's premium.

| Year | Standard Part B premium | What changed that year |

|---|---|---|

| 1966 | $3.00 | Medicare Part B launches at $3.00/month under the 1965 Social Security Amendments |

| 1970 | $5.30 | |

| 1975 | $6.70 | |

| 1980 | $9.60 | |

| 1985 | $15.50 | |

| 1990 | $28.60 | |

| 1995 | $46.10 | |

| 2000 | $45.50 | |

| 2005 | $78.20 | |

| 2010 | $110.50 | |

| 2015 | $104.90 | |

| 2016 | $121.80 | |

| 2020 | $144.60 | IRMAA income brackets indexed to inflation for the first time since 2007 |

| 2021 | $148.50 | |

| 2022 | $170.10 | |

| 2023 | $164.90 | Part B premium falls 3% after the 2022 Aduhelm reserve proves unnecessary |

| 2024 | $174.70 | |

| 2025 | $185.00 | |

| 2026 | $202.90 | CMS sets the standard Part B premium at $202.90 and deductible at $283 |

Full series shown. Scroll within the table to see every year.

Frequently Asked Questions

What is the 2026 standard Medicare Part B premium?

How does the IRMAA two-year lookback work?

Is IRMAA a marginal surcharge or a cliff?

Can I appeal or reduce my IRMAA surcharge?

Why did the Medicare Part B premium drop in 2023?

What is the difference between Part B and Part D IRMAA?

For the top-tier IRMAA surcharge charted on its own, see IRMAA bracket history. To model the income that drives your tier, the retirement calculator and the Roth vs Traditional comparison both bear on the conversion timing question. For sources and update cadence, see our methodology.

Related Calculators

IRMAA Bracket History

The top-tier Part B surcharge over time, with the underlying legislation charted.

Retirement Calculator

Stress-test a drawdown plan, including the income that drives your IRMAA tier.

Roth IRA vs Traditional IRA

Conversions raise MAGI and can trip an IRMAA bracket two years later.

Tax Bracket Calculator

See how MAGI stacks against ordinary brackets in a conversion year.

Social Security COLA History

The annual raise that partly offsets Part B premium increases.

Methodology

How we source and verify every rate, limit, and bracket.

Educational content only. The 2026 premium, deductible, and IRMAA amounts shown here are the final amounts CMS announced on November 14, 2025. Medicare amounts are set annually; consult CMS, Social Security, or a qualified advisor for decisions specific to your situation.